A better way so you can Calculate a keen Amortization Plan

So you’re able to calculate the following month’s desire and dominating payments, subtract the principal percentage produced in times you to ($) regarding financing balance ($250,000) to discover the this new mortgage balance ($249,), following repeat the fresh new procedures significantly more than to help you determine hence part of the second percentage is allocated to attract and you may that’s designated to the prominent. You can recite these tips if you don’t have created an enthusiastic amortization plan to the complete longevity of the loan.

Figuring an amortization schedule is as simple as going into the principal, interest, and you will loan identity to the financing amortization calculator. But you can and additionally estimate it manually if you know the interest rate for the financing, the principal amount borrowed, additionally the mortgage label.

Amortization tables usually were a line to own scheduled money, focus expenses, and you will dominant installment. While causing your individual amortization schedule and you will decide to make any even more dominating repayments, just be sure to create an additional range for it items to be the cause of even more transform on loan’s a good balance.

How exactly to Calculate the total Monthly payment

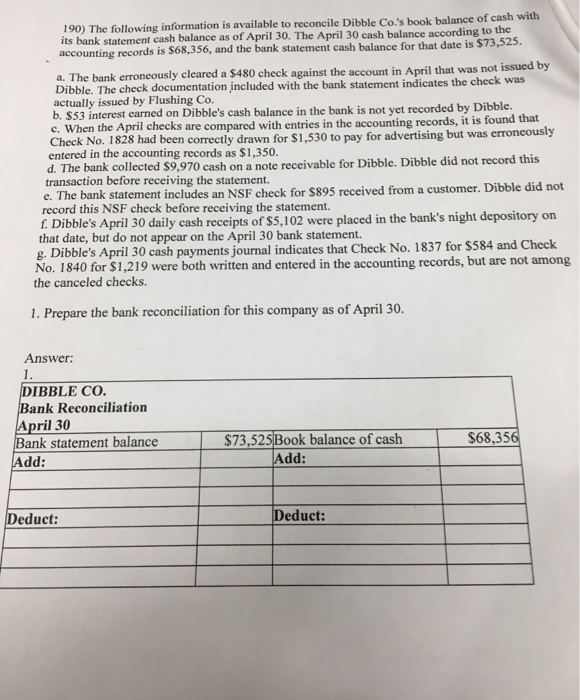

![]()

Generally speaking, the full payment per month try given by your financial when you sign up for financing. Although not, while you are trying to imagine otherwise compare monthly obligations established for the a given band of activities, instance loan amount and interest rate, you may need to determine brand new payment too.

- we = month-to-month interest. You’ll need to divide the annual interest by the twelve. Like, in the event the annual rate of interest is six%, their monthly interest rate might possibly be .005 (.06 annual interest / 12 months).

- letter = amount of money over the loan’s existence. Proliferate just how many many years on your own financing label by twelve. Particularly, a 30-year mortgage might have 360 repayments (30 years x 12 months).

Using the same analogy away from more than, we shall assess the latest payment with the an excellent $250,000 mortgage with a thirty-seasons name and you can a cuatro.5% interest rate. The newest picture provides $250,100000 [(0.00375 (step one.00375) ^ 360) / ((step one.00375) ^ 360) – step 1) ] = $step 1,. The result is the payment per month due on financing, together with both dominant and you may appeal charges.

30-Year against. 15-Seasons Amortization Desk

If a borrower determines a shorter amortization period because of their home loan-such as for example, 15 years-they rescue more into the focus over the lifetime of new loan, and they’ll individual our home eventually. This is because might generate fewer costs whereby attract might be amortized. Simultaneously, rates of interest towards the smaller-name fund are for a cheap price versus offered-label finance.

Discover a great tradeoff, although not. A shorter amortization screen escalates the payment per month owed toward financing. Quick amortization mortgages are good alternatives for consumers who will deal with large monthly payments in the place of difficulty; it nonetheless encompass making 180 sequential payments (15 years x 12 months).

It is vital to thought even in the event you can take care of you to definitely level of fee centered on your money and you will budget.

Having fun with a keen amortization calculator helps you examine mortgage payments facing prospective focus deals to have a smaller amortization to determine and that alternative suits you better. Here’s what an excellent $five hundred,100 mortgage having an excellent 6% rate of interest carry out appear to be, having a hypothetical 30-seasons and 15-12 months agenda to compare:

Refinancing away from a 30-seasons loan in order to a fifteen-season home loan can save you cash on attention charge however, whether it will or perhaps not depends on how much of one’s modern loan’s focus you have already paid off.

What is actually a thirty-Seasons Amortization Agenda?

An 30-season amortization agenda stops working how much cash away from a level fee into that loan goes toward often prominent or appeal along the span of 360 weeks (age.g., towards the a 30-12 months financial). Early in living of your mortgage, every loans Addison AL payment per month would go to interest, when you’re into the finish it’s mostly comprised of dominating. It may be displayed either given that a dining table or in graphical mode just like the a map.

Sin comentarios